Water is squeezed out of a Stone

Lemon juice can be squeezed out of lemons and orange juice from oranges but it is impossible to squeeze water out of a stone - usually. There are exceptions to every rule! In this case, John Bosco of the law firm of Bosco, Bisignano & Mascolo, Esqs. LLP succeeded in squeezing water out of an ordinary stone on behalf of their seriously injured client. Caution: What appears to be legal magic is the result of decades of experience in practicing personal injury law. Do not try this trick yourself or with an ordinary lawyer.

Lemon juice can be squeezed out of lemons and orange juice from oranges but it is impossible to squeeze water out of a stone - usually. There are exceptions to every rule! In this case, John Bosco of the law firm of Bosco, Bisignano & Mascolo, Esqs. LLP succeeded in squeezing water out of an ordinary stone on behalf of their seriously injured client. Caution: What appears to be legal magic is the result of decades of experience in practicing personal injury law. Do not try this trick yourself or with an ordinary lawyer.

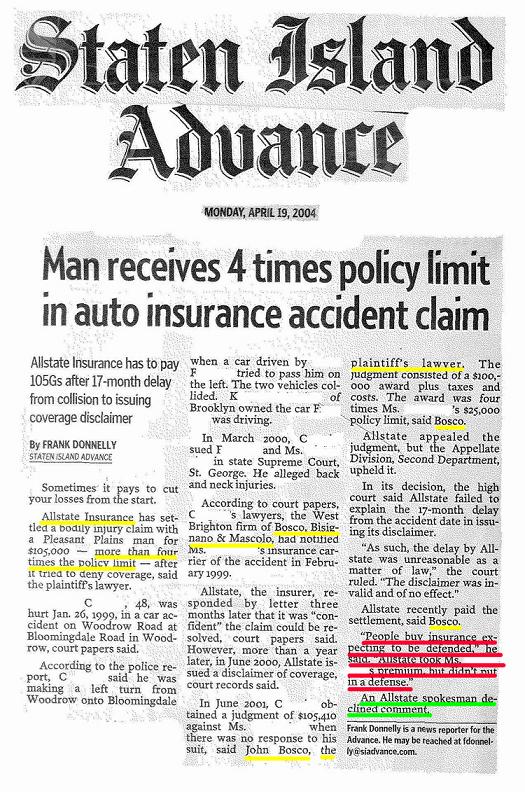

John Bosco's client came to them after having been injured in a car accident. John Bosco has computer access to the records of the New York State Department of Motor Vehicles. Consulting them, John Bosco learned that the DMV's records listed Allstate as the Insurance Company for the car that struck their client. John Bosco contacted Allstate who told him that Allstate provided only $25,000/$50,000 in liability insurance. This meant that there was only $25,000 available to our seriously injured client.

The first number in a dual limit liability policy is the most an Insurance Company will pay to any individual hurt in an accident. The second number is the most an Insurance Company will pay to all individuals hurt in an accident. To an individual, it is the first number that counts and that's why only $25,000 was available to our client under a 25/50 policy.

A 25/50 policy is the minimum amount of insurance that New York State requires for its drivers with a few exceptions. To protect yourself from such underinsured drivers it is important that you review your own car insurance policies to make sure you have sufficient uninsurance and underinsurance coverage. Un and Under insurance protects you when you are injured by a car that has no insurance or too little insurance to fairly compensate you for your injuries. When you purchase a car liability insurance policy, you are purchasing coverage that will benefit others. Un and Under insurance is one of the coverages that protects you and your family. Don't overlook it. Get enough of it because there are too many bad drivers using our roads with either no or too little insurance.

Meanwhile, back to our story.

After John Bosco contacted Allstate, Allstate investigated the accident and thought some shenanigans were going on involving their driver and owner so Allstate disclaimed. Allstate told John Bosco that they would not honor their obligation under the insurance policy that it issued. Our client had only $25,000 in underinsurance coverage through his own policy.

John Bosco did not like the idea that Allstate was refusing to honor its policy so he took action. John Bosco, using his decades of experience representing the victims of auto accidents, took advantage of a mistake Allstate made. Allstate disclaimed and refused to both indemnify and defend its insured. Allstate, however, ought to have disclaimed, defended, and simultaneously brought a declaratory judgment action to get the Court's approval of their refusal to defend and indemnify. By failing to follow the proper procedure, John Bosco was able to take advantage of Allstate's mistake.

John Bosco first took a default judgment against the Allstate vehicle. Remember Allstate had refused to defend it. The default judgment was for an amount approximately four times (4x) greater than Allstate's 25K policy. Then John Bosco started a legal proceeding seeking benefits under our client's 25K uninsured policy. In that proceeding, our client's insurer and Allstate were made a party. At the conclusion of that proceeding, the Court determined that Allstate had mistakenly disclaimed its obligation under its policy. Allstate indeed had the duty to indemnify and defend. But now it was too late. John Bosco already had a default judgment for an amount four times (4x) greater than the Allstate $25,000 policy. Allstate had made a costly mistake. Thanks to the good lawyering of John Bosco, Allstate's mistake benefited our client to the tune of four times the available insurance coverage. Instead of getting only $25,000, John Bosco's happy client received approximately four times as much.

John Bosco

John Bosco